Content

For example, the total payments required by the modified contract must be substantially the same as, or less than, the total payments required by the original contract. Thus, incentives such as tenant allowances are a very common book/tax difference. Under the new GAAP standard, taxpayers also face a potentially burdensome tracking issue to reconcile the incentive book/tax differences now that the incentives are buried in the right-of-use asset.

MULLEN AUTOMOTIVE INC. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. (form 10-K) – Marketscreener.com

MULLEN AUTOMOTIVE INC. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. (form 10-K).

Posted: Fri, 13 Jan 2023 08:00:00 GMT [source]

Marcum LLP is a national accounting and advisory services firm dedicated to helping entrepreneurial, middle-market companies and high net worth individuals achieve their goals. Since 1951, clients have chosen Marcum for our insightful guidance in helping them Deferred Rent Tax Treatment for Accounting under Current GAAP forge pathways to success, whatever challenges they’re facing. However, there are certain safe harbors, such as Section 110, which allow for the lessee to exclude the incentive from income to the extent it is used to construct real property improvements.

Example #2: Deferred rent under ASC 842 with ROU assets and lease liabilities

Transfer pricing is used by entities to determine the appropriate amount to charge for intercompany transactions. While these types of transactions are eliminated when consolidating for book purposes, they are not eliminated in each taxing jurisdiction for tax purposes. When making the decision as to the right basis of accounting for your real estate firm, consult with a professional. Divide the total rental cost by the total number of periods in the lease contract including the free rental month.

How do you account for deferred rent?

What is the Accounting for Deferred Rent? Accounting for the free rent period and subsequent periods are as follows: Add the total cost of the rent payments for the entire lease period. Then divide this total amount of payments by the total number of periods in the lease, including any early access period.

The following example illustrates the treatment of initial direct cost and deferred rent, the latter of which is no longer recognized for balance sheet purposes. The chart “Accounting at Lease Commencement Date” illustrates amortization of the right-of-use asset and the lease liability, as well as related journal entries. Using the data in the table “Expense and Amortization Schedule,” a lessee would make the journal entries shown in that chart. This entry records the operating lease and payment of initial direct cost at the commencement date. When we study the effects of ASC 842, we believe that the balance sheet assets and liabilities will increase accounts evenly for the most part, without impacting the income statement. For operating leases, the new lease standard will generally result in a constant annual cost similar to the expense pattern under current operating lease accounting.

Accounting for Deferred Expenses

Most of the dialogue, articles, CPE courses, etc. have concentrated on the GAAP rules and reporting requirements. As a result, some of the tax impacts of the new standard have not been fully considered. One common example relates to the depreciation deduction since the IRS allows for accelerated depreciation and other special depreciation. (We discussed this in the installment Scary Word No. 6 – PPE.) This temporary difference means paying fewer taxes in the present. It does not mean you won’t pay the taxes eventually; it means that you will pay them during a future period. Deferred rent describes the difference between your monthly rent payment and your actual rent expense.

RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a global network of independent audit, tax and consulting firms. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmus.com/about for more information regarding RSM US LLP and RSM International. Divide this amount by the total number of periods covered by the lease, including all free occupancy months. To continue with the same example, this would be $917, which is calculated as $11,000 divided by 12 months. These include white papers, government data, original reporting, and interviews with industry experts.

Why Do Deferred Tax Assets Occur?

2.“An entity need not reassess the lease classification for any expired or existing leases.” Thus, leases classified as operating leases under Topic 840 may continue as operating leases under Topic 842. This post is published to spread the love of GAAP and provided for informational purposes only. Although we are CPAs and have made every effort to ensure the factual accuracy of the post as of the date it was published, we are not responsible for your ultimate compliance with accounting or auditing standards and you agree not to hold us responsible for such. In addition, we take no responsibility for updating old posts, but may do so from time to time.

- As a result of transitioning to ASC 842, organizations will see an increase in overall liability and asset balances, which may significantly impact the balance sheet and financial ratios used by various stakeholders.

- Before, it was easy to see the impact of straight-line rent in the deferred rent account.

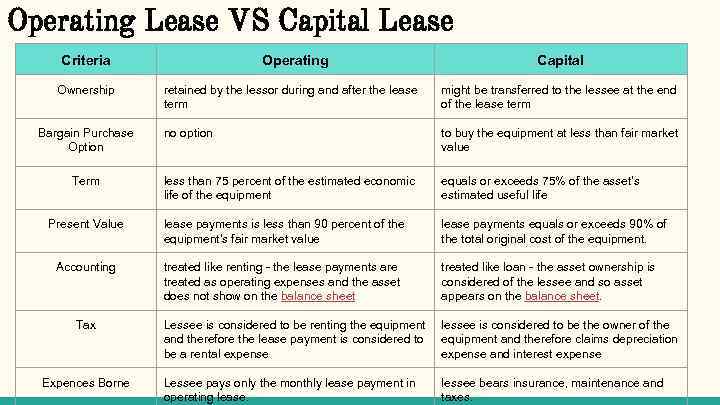

- As was the case under ASC 840, rent expense is not reported on the balance sheet.

- The lessor generally capitalizes the tenant improvement allowance and amortizes it over the term of the lease.

- The FASB staff noted there could be multiple approaches to accounting for deferrals under both ASC 842 and ASC 840.

Franchise taxes are generally based upon the net worth (stockholder’s equity) of a corporation; however, various adjustments may be required (e.g., treasury stock, liabilities, reserves, etc.) to arrive at the taxable base. Implementation of the new leasing standard may impact the computation of a company’s franchise tax base, due to the requirement to record essentially all leasing transactions on the balance sheet for financial accounting purposes. Moreover, the property factor utilized in the computation of many state apportionment factors is determined through the use of an average owned property and eight times the net annual rent. After the adoption of ASC 842, companies may need to change the process used to gather information for property factor computations, particularly if the right-of-use asset is recorded in the same balance sheet account or line item as other owned property.

Assurance Services

For companies, location is everything, especially for real estate and retail companies. It’s important to be located in a place with a lot of foot traffic and access to the company’s target consumer base. Companies often allocate a large part of their rental expense towards prime locations. For such companies, it’s crucial to weigh the cost of the rent against the benefits and potential boost in revenue that comes from being in a prime location. As companies prepare to adopt the new lease accounting standard, tax implications and opportunities should be considered at each step of the implementation process.

- This difference is used to reduce the amount of the deferred rent liability over the remaining months of the lease, until it is reduced to zero.

- These rules are located at Section 467 of the Code1 and its accompanying regulations.

- This makes the accounting easier, but isn’t so great for matching income and expenses.

- Because the characterization of an operating lease is that the lessee is not the economic owner of the underlying asset, there was no balance sheet interaction.

GAAP. This deferral of profit may create new deferred tax assets since those leases will typically be non-tax leases for tax purposes. Under tax law, the entire profit on the lease (sales price – tax basis of the asset) will be recognized for tax purposes at the time of the sale. In the example, the charge to Income Statement for initial years will be higher and will reduce in the later period of a lease. This will lead to the creation of temporary difference for an operating https://online-accounting.net/ lease given the change in GAAP accounting. The differences between the GAAP and tax basis of the ROU asset and related lease liability will result in taxable income or deductions upon their reversal; such differences are temporary in nature. From a lessee’s perspective, the most significant change from prior lease guidance is that lessees are required to recognize the rights and obligations resulting from most operating leases as assets and liabilities on their balance sheet.

As a result, lease liabilities, which represent the present value of the lessee’s future obligations, and right-of-use assets, which represent the lessee’s rights to use the underlying assets, are recorded at lease commencement. Under the income tax basis, real estate assets are depreciated over periods specified in the Internal Revenue Code, while GAAP uses estimated useful lives. The income tax basis allows for accelerated depreciation methods, while GAAP traditionally depreciates over the applicable lives on a straight line basis. Consider instead an example not from the regulations promulgated under Section 467 of the Code, but which includes certain circumstances lessors and lessees may encounter in today’s environment. In this example, there is initially a five-year lease that provides both for accrual and payment of $100,000 of rent per year. In Y2, there is an economic downturn, and to accommodate the financial straits of the lessee, the lessor and lessee amend the lease to defer the rent originally due in Y2 and Y3 to be amortized over Y4 and Y5.

What is the journal entry for unearned rent?

Unearned revenue should be entered into your journal as a credit to the unearned revenue account, and a debit to the cash account. This journal entry illustrates that the business has received cash for a service, but it has been earned on credit, a prepayment for future goods or services rendered.